When considering any kind of borrowing in Nigeria, especially a business loan, it’s highly important to know and understand the real cost of such loan. That is, you should understand what the businessloan will cost you with time.

Loanis a pretty simple term. It is simply borrowing money and then repaying it. However, the amount you will repayis more than what you borrowed. The primary reason for this increase is the fees and interest charged by the lender for lending out its money to you. Generally, apart from interest and interest rates, there are several things that are associated with borrowing. These have been briefly explained below.

Interest and Interest Rate — The True Cost of Borrowing

Interest is the price paid by borrowers to the lenders. Interestrate is the cost of borrowing which is normally expressed as a percentage of the money borrowed (referred to as principal). Precisely, it’s the percentage of the principalthat you will pay over a particular and agreed period of time. There are several kinds of interest rate commonly charged on loans in Nigeria. They include simple (flat) interest rate, compound interest rate, reducing balance rate, flat interest rate andannual percentage rate.

Simple interest rate (also known as flatinterest rate)is the most basic interest rate. Simple Interest is the interest charged on the principal (or money borrowed) throughout the tenor of the loan. It doesn’t change and it is paid once. Simple interest is calculated using this formula: I = P x R x T, where P= Principal, T=term and R= interestrate. For instance, if you borrow ₦500,000 from a bank, at 20% rate and for 1½ years, the simple interest equals ₦150,000 (i.e. ₦500,000 x 0.2 x 1.5). This means you’re expected to pay ₦650,000 to that bank.

For compound interest rate, interest is charged on the principal amount borrowed and on the previous interest. The compound interest is computed using this formula:

CI= (P(1 + r/n) ^ nt) — P),

where P= Principal, r= interest rate, n= number of compounding period in a year and t is the loan term or tenor.

Using the previous example where n is 1 year, the compound interest will be:

CI = ₦(500,000 (1 + 0.2/1) ^ (1 x 1.5)) — ₦500,000

CI = ₦(500,000 (1.2) ^ 1.5)) — ₦500,000

CI = ₦(500,000 * 1.31) — ₦500,000

CI = ₦655,000 — ₦500,000

CI= ₦155,000

Reducing balance ratecharges interest only on the remaining or outstanding balance of a loan. In this case, you will be paying lower interest on the principal every month as you settle the principalitself. The formula for computing reducing balance interest is:

Interest amount per installment = Interest rate per installment x Outstanding loan amount

Annual percentage rate (APR) is the interest rate on your loan for one whole year. Practically, it is the true cost of your loan because it includes the interest rate charged by the lender and other fees incurred or collected at the time the loan is given.

Other Fees

Besides interest, there are some lenders or banks that charge additional fees to the loans they give out. Generally, these extra fees are a percentage of the principal that is deducted from what is received by the borrower. The lender usually charges these fees immediately the borrower receives the loan. For instance, if the lender assesses a 3% fee on your ₦1,000,000 business loan, the fee on the loan is ₦30,000 and you will be given ₦970,000. However, you will still have to pay back the ₦1,000,000 as well as the associated loan interest to the lender.

Other fees charged by lenders that you should know include loan arrangement or processing fees, late payment charges, early redemption fees, transaction fees, loan deferment andforbearance fees, and agreement fees. Even though it’s not all lenders that charge these additional loan fees, it’s important for you as a borrower to know and understand all the fees associated with your business loan. All the terms of your loan and associated fees are always included in the credit agreement. This is why it’s important for you to read this document carefully to know the othercosts associated with the loan.

Equity Contributions

Business loans usually require equity contributions from the business owners. For example, when you apply for a business loan, the business lender may request for financial statements that show the whole project cost. Afterward, the lender will give you a certain percentage of the money you want to borrow, requiring you to contribute the remaining percentage. The objective of the lender, in this case, is that they want you as the business owner to have your own money at risk along with its own money. The equity can range from as low as 10% to as high as 50%. This is usually determined by the type of loan, what the loan will be used for or the Lender’s policies.

Loan Affordability

Before lenders give out their money, they usually determine if a borrower can afford to repay the loan he/she applied for or how much he/she could borrow considering a number of factors. Loan affordability is determined after assessing monthly gross income and expenditure, loan interest rate and loan tenor or term. After determining your loan affordability, the lender or loan provider will determine if they should give you the loan or not. For business loans lenders will usually look at your surplus cashflow/profit to determine/assess your affordability and they will usually user 33.3% of this as your maximum monthly loan repayment, this can differ from Lenders to lenders as it is determined ultimately by the Lenders risk appetite and underwriting policies.

Loan Tenor, Equated Monthly Installment and Amortization Schedule

Loan tenor (or tenure) is simply the amount of time left to repay a loan. It is also the period from the date a loan is disbursed to the date of loan closure or last equated monthly installment (EMI). As the year passes, the loan tenor reduces.

On the other hand, Equated Monthly Installment (EMI)is the fixed amount of money a borrower must pay to a lender at a specified day in each month. EMI payments are monthly contributions towards the principal and interest on the loan until the loan is paid off in full. The formula for computing EMI is:

EMI = P × R × (1 + r)n/((1 + r)n — 1);

where P= Loan amount, r= interest rate, n=loan tenure in months.

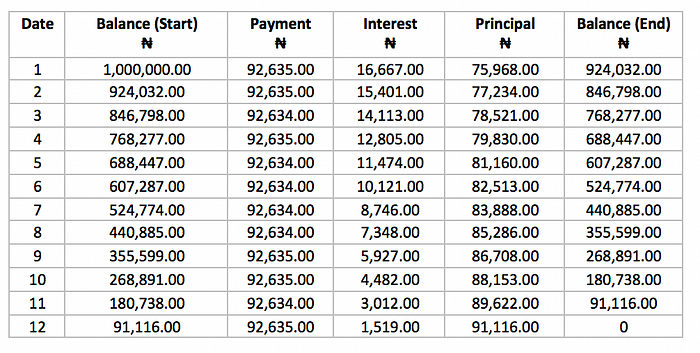

EMI payments are included on the loan amortization schedule. A loan amortization schedule (also called amortization table) is a table showing the beginning and end of a loan as well as the EMI payments. The table clearly breaks up the EMI payments into principal and interest and it also reveals other components of a loan. Hence, it makes it easy for a borrower to know how much has been paid and the amount that is yet to be balanced or paid. An amortization table will allow you to figure out the real cost of borrowing as you will be able to see what you really pay in interest on a loan. The table below is an example of an amortization schedule for a ₦1,000,000 business loan with a 20% interest rate on a reducing balance and 1-year loan tenor.